myfinquest

TF Buzz

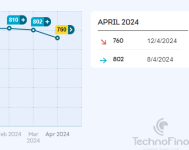

My CIBIL score was 810 in March. Today, I was surprised to see it at 760. There were no new accounts , but two disputes I raised

1. Mark Barclay's credit card as closed. (Barclays closed down in India in 2012). This was not my oldest card

2. Mark HDFC car loan (paid up in Aug 2023) as closed.

Will the above causes a drop of 50 ? I don't think so. I had to raise multiple disputes to get the Barclays cc to be marked as closed and I gave multiple bad ratings to their surveys as well.

I have a new HDFC car loan , but it is yet to be reflected in CIBIL report. The only significant thing happened recently was in early Feb when I got an unsolicited loan enquiry from EArly Salary. Though I disputed this with CIBIL , complained with RBI, nothing happened. Early Salary says they got an enquiry through WeCredit and WeCredit says they got it from one of their partners which they are not divulging. But, this caused a drop of only 5 points from Feb to March.

Anyone seeing such massive changes to CIIBL scores ? Wondering if there is any change in the score calculation rules from new financial year.

Thanks.

1. Mark Barclay's credit card as closed. (Barclays closed down in India in 2012). This was not my oldest card

2. Mark HDFC car loan (paid up in Aug 2023) as closed.

Will the above causes a drop of 50 ? I don't think so. I had to raise multiple disputes to get the Barclays cc to be marked as closed and I gave multiple bad ratings to their surveys as well.

I have a new HDFC car loan , but it is yet to be reflected in CIBIL report. The only significant thing happened recently was in early Feb when I got an unsolicited loan enquiry from EArly Salary. Though I disputed this with CIBIL , complained with RBI, nothing happened. Early Salary says they got an enquiry through WeCredit and WeCredit says they got it from one of their partners which they are not divulging. But, this caused a drop of only 5 points from Feb to March.

Anyone seeing such massive changes to CIIBL scores ? Wondering if there is any change in the score calculation rules from new financial year.

Thanks.