CHOCOPANDA

TF Premier

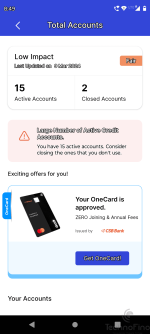

I saw this message in one score app. It is recommending to close some cards which I don't use. So I have sent email to bank to close them. Thelist is followed. I am thinking to increase my cibil score but it is going down and reached 769 from 774. As in near future I would take home loan. So what will be the consequences of this cibil score. My experon score has also gone down by 28 points and reached 798 from 826.

Someone has suggested me that many credit card shows to bank this person is credit hungry and is fully dependent on it. So taking this decision.

I have closed

Axis Flipkart recently

And now will close

Bob easy virtual rupay

Standard chartered platinum rewards credit card

RblShopriteLtf

ICICI platinum chip

ICICI Coral rupay

Au altura

Will the bulk closure improve my score or it will hamper it more?

Someone has suggested me that many credit card shows to bank this person is credit hungry and is fully dependent on it. So taking this decision.

I have closed

Axis Flipkart recently

And now will close

Bob easy virtual rupay

Standard chartered platinum rewards credit card

RblShopriteLtf

ICICI platinum chip

ICICI Coral rupay

Au altura

Will the bulk closure improve my score or it will hamper it more?

Attachments

Last edited: