Navigation

Install the app

How to install the app on iOS

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: This feature may not be available in some browsers.

More options

Style variation

-

Hey there! Welcome to TFC! View fewer ads on the website just by signing up on TF Community.

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Cibil defaults wipe off?

- Thread starter cardex

- Start date

- Replies 90

- Views 7K

-

- Tags

- cibil cibil report

There are 2 summaries in CIBIL for 3 years and 7 year period. After 7 years there should not be any impact.I heard it gets wiped off after 7 years?

Banks issue cards even after defaults.Default marking remains for forever. After 7 years, if your other CC records are good and cibil score is above 750, some bank may give you new cc. keep your finger crossed.

Depends on many other factors as well.

sumitlehri

TF Buzz

Yeah even i pay 10 20 ruppee extra but i dont know how i missed this time..I called customer care and raised request but he was not sure of cibil..Mailed on all hdfc email id.Lets see how it would turn outThey ideally should not though you should write and also talk to their phone banker immediately. But in past it has been seen in some incidences that they have reported it. That's why I tend to round up to the higher payable rupee.

All the best. I'm sure they would understand that it happened inadvertently and no one would default for 0.36. They can suppress the information 😊Yeah even i pay 10 20 ruppee extra but i dont know how i missed this time..I called customer care and raised request but he was not sure of cibil..Mailed on all hdfc email id.Lets see how it would turn out

All can be expected to oblige except SbicardsAll the best. I'm sure they would understand that it happened inadvertently and no one would default for 0.36. They can suppress the information 😊

Correct. Most do, some will not until you have high NRV/TRV with them, Axis, Federal, Stan C comes to mind straight away. They will keep rejecting applications stating the same old "internal policy" nonsense.Banks issue cards even after defaults.

Depends on many other factors as well.

Off topic, RBI should give more stricter directives to the banks to disclose reasons for CC rejections, So that one can rectify those reason for rejections if possible or just stop applying with the same bank if the reason stated for the rejection is beyond their control. Most banks UK / USA abroad do it, so no reason why Indians banks cannot do the same.

me too confirmed it from CIBIL, they said we are only able to erase it after 7 years of closing date so, till that date you have to bear the consequences.I heard it gets wiped off after 7 years?

this is not true, from the same year onwards you can start with a secured credit card and then request bank to give you credit card most likely the chances are they will give it you. Initially, you'll a low limit card but you can build on that limit so, after 3-4 years of 0 late payments you'll start getting high credit limits.Default marking remains for forever. After 7 years, if your other CC records are good and cibil score is above 750, some bank may give you new cc. keep your finger crossed.

Au

Surprised to see Axis in the list. I guess because the loan was settled & not a write-off !I settled an edu loan but still got all many cards after settling.

3 ICICI, 3 HDFC, 1 Axis, 1 SBI.

I got all cards I applied for.

The person from CIBIL who said it must have been really high on weed or didn’t know what he was talking about.CIBIL, they said we are only able to erase it after 7 years of closing date

ALL loan / CC account (irrespective of the status i.e closed/settled/defaulted) drops of from Experian on the 7th year.

Accounts once reported in TRANSUNION-CIBIL stays in the report “FOREVER”, irrespective of its status.

Period.

ravipr

TF Buzz

Au

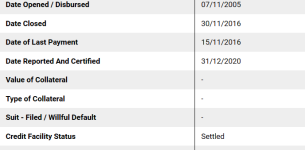

Surprised to see Axis in the list. I guess because the loan was settled & not a write-off

Yes I guess. Report says "Written off status: Settled"Au

Surprised to see Axis in the list. I guess because the loan was settled & not a write-off !

ravipr

TF Buzz

Btw a question is can I pay and close that settled loan now? Will that remove the settled mark? Does anyone have any experience regarding this?Yes I guess. Report says "Written off status: Settled"

Correct. If you would not have settled paying a certain amount to the bank, the Written-off status would have read "write-off / Wilful default / default".Yes I guess. Report says "Written off status: Settled"

Absolutely. Have you ever seen anywhere in the world where a bank says "NO" to money ? If it is a sarkari bank you might have to visit the loan processing centre to pay it off & collect the acknowledgement / receipt, however in case of a private bank just write them an email, take the confirmation, pay however you wish, receive the NOC & wait 45-60 days in that order & you will the the write-off in CIBIL has changed to closed & per se there is NO time limit to do this & if the bank refuses / is reluctant, get the RBI ombudsman involved straight away !Btw a question is can I pay and close that settled loan now? Will that remove the settled mark? Does anyone have any experience regarding this?

However, am curious why do you want to do this if you're getting approved for everything !?

cardex

TF Premier

After? Settlement date? Default date?There are 2 summaries in CIBIL for 3 years and 7 year period. After 7 years there should not be any impact.

As far as DPDs are concerned there are two summaries, 1 & 3 years ! Cibil keep records of DPDs for upto 3 years & lifetime for any credit account.There are 2 summaries in CIBIL for 3 years and 7 year period. After 7 years there should not be any impact.

So if you have made a late payment & the account is active for the next 36 months, then the DPD reflecting the late payment will fall off & it will seem as if you never had a late payment on the account, however if the account is closed before 36 months from the late payment date, then the late payment DPD will continue to reflect for a lifetime !

If you “settle” any credit account or are late with your payments then the effect will be negligible after 3-4 years, provided you need to have some other credit accounts open in cibil with NO further late payments on those.

However, if the account status is default / wilful-default then get ready to wait for at least 7-8 years before getting fresh credit, subject to one having other previous credit accounts still open in cibil & makes no further late payments on those.

That is how CIBIL works & hence some lenders pick up defaults someone made even 15 years back & may still ask questions for a big ticket loan !

Last edited:

ravipr

TF Buzz

My CIBIL is 798, experian 840 even with the Settled mark. They are giving me CC's immediately and I have plenty now.Absolutely. Have you ever seen anywhere in the world where a bank says "NO" to money ? If it is a sarkari bank you might have to visit the loan processing centre to pay it off & collect the acknowledgement / receipt, however in case of a private bank just write them an email, take the confirmation, pay however you wish, receive the NOC & wait 45-60 days in that order & you will the the write-off in CIBIL has changed to closed & per se there is NO time limit to do this & if the bank refuses / is reluctant, get the RBI ombudsman involved straight away !

However, am curious why do you want to do this if you're getting approved for everything !?

But I know in a year or so I will need to get home loan and I feel then the settled remark will cause some issue.

Connect with a bank of your choice from which you woukd lik le to take this home loan & check if they have an issue after sharing CIBIL reportMy CIBIL is 798, experian 840 even with the Settled mark. They are giving me CC's immediately and I have plenty now.

But I know in a year or so I will need to get home loan and I feel then the settled remark will cause some issue.

Last edited:

Yes - status will get updated as Closed incase you pay the full pending amount.Btw a question is can I pay and close that settled loan now? Will that remove the settled mark? Does anyone have any experience regarding this?

Similar threads

- Replies

- 6

- Views

- 160

- Replies

- 12

- Views

- 988

- Replies

- 1

- Views

- 197

- Replies

- 10

- Views

- 473

- Question

- Replies

- 17

- Views

- 711