Hello Community,

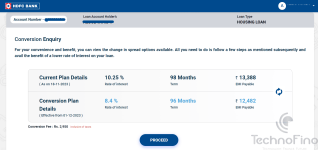

I have a home loan with HDFC Bank with current Rate of Interest 9.25%.

Recently I had a call with HDFC home loan customer care and they offered me a interest rate of 8.35% with a conversion fee of rupees 5900.

Some folks suggested that the fee can also be waived off, if it is possible how may I do it? The branch is in a different city and I don't have any interaction with the branch manager.

I have a home loan with HDFC Bank with current Rate of Interest 9.25%.

Recently I had a call with HDFC home loan customer care and they offered me a interest rate of 8.35% with a conversion fee of rupees 5900.

Some folks suggested that the fee can also be waived off, if it is possible how may I do it? The branch is in a different city and I don't have any interaction with the branch manager.