viru5678

TF Select

Recently I transferred my Home Loan from HDFC to HSBC. Below are some of the key points which made my decision.

One of my colleague holding HSBC home loan since last 5 years helped me lot with decision making and giving some important insights around HDFC RPLR vs HSBC RLLR

1. Overall ROI - Overall HSBC gave me better return on Home Loan.

I started my HDFC Home during JUl-2021 @ 7% Interest Rate and frequently rates were hiked till 8.55% by Feb-2023.

I have seen HDFC increasing rates even when there were no changes to RRLR by RBI.

Jul-2021 : Interest rates @ 7% -

Jan-2023 : Interest Rate @ 8.55% -

2. Criteria of Interest Rates - Overall I found HSBC is transparent with Interest Rate criteria and linking with RBI Repo Rate

HDFC follows RPLR - Retail Prime Lending Rate :-

- For customers this is not directly linked with RBI Repo rate and HDFC reviews periodically (criteria not known to me)

- I have seen HDFC increaing rates every two months and never reduced rate on their own.

- In order to reduce Interest rate you need to keep checking and keep bugging customer care. Now HDFC will reduce rate by charging you some fee.

- As per my experience HDFC raised rates even when RBIs Repo rate was constant.

- There was no change in EMI but bank sliently kept increasing overall tenure.

HSBC followes RLLR - Repo Linked Lending Rate :-

- RLLR is directly linked with RBI Repor rate published every month.

- RLLR is reviewed monthly and bank makes changes accordingly - upward or downward.

- There is no additional fee required if Interest rate goes down.

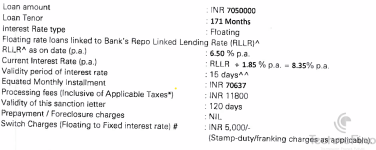

Below is the snap shot of Home Loan sanction by HSBC:

Some important terms and conditions: HDFC does not state any linkage with RBI repo rate where as HSBC has given interest rate calculation in black and white.

3. Home Loan Switching Charges: ( I have already received refund)

All the charges except procesing fee (around 9000) were refunded by HSBC and Loan Processing agency. They gave me in writing what will be refunded and when.

4. Overall process experience

Home Loan processing expereince with either HDFC or HSBC is very smooth and no hasseles at all. HSBC only looks for higher CIBIL score.

Process of closing Home Loan with HDFC was smooth. They offered lower interest rate only upon closure application.

HDFC also refused to link Interest rates with RBI Repo rate and they said they do not follow this process.

Home Loan switching with HSBC was also smooth and I never visited their branch.

I can share and influence HSBC agency contacts if anyone wants to switch the loan. Keep in mind good Cibil will give you lower rates and rest of the conditions remains same.

If you are from Pune then I can share some direct HSBC contacts who can make this process butter smooth for you.

Considering all the factors and hacing seen my colleagues expereince with HSBC I switched my Home Loan.

Now I have freed myself from the worries of moving interest rates, keeping watch every month and paying extra changes to HDFC for lowering the rates.

One of my colleague holding HSBC home loan since last 5 years helped me lot with decision making and giving some important insights around HDFC RPLR vs HSBC RLLR

1. Overall ROI - Overall HSBC gave me better return on Home Loan.

I started my HDFC Home during JUl-2021 @ 7% Interest Rate and frequently rates were hiked till 8.55% by Feb-2023.

I have seen HDFC increasing rates even when there were no changes to RRLR by RBI.

Jul-2021 : Interest rates @ 7% -

Jan-2023 : Interest Rate @ 8.55% -

2. Criteria of Interest Rates - Overall I found HSBC is transparent with Interest Rate criteria and linking with RBI Repo Rate

HDFC follows RPLR - Retail Prime Lending Rate :-

- For customers this is not directly linked with RBI Repo rate and HDFC reviews periodically (criteria not known to me)

- I have seen HDFC increaing rates every two months and never reduced rate on their own.

- In order to reduce Interest rate you need to keep checking and keep bugging customer care. Now HDFC will reduce rate by charging you some fee.

- As per my experience HDFC raised rates even when RBIs Repo rate was constant.

- There was no change in EMI but bank sliently kept increasing overall tenure.

HSBC followes RLLR - Repo Linked Lending Rate :-

- RLLR is directly linked with RBI Repor rate published every month.

- RLLR is reviewed monthly and bank makes changes accordingly - upward or downward.

- There is no additional fee required if Interest rate goes down.

Below is the snap shot of Home Loan sanction by HSBC:

Some important terms and conditions: HDFC does not state any linkage with RBI repo rate where as HSBC has given interest rate calculation in black and white.

3. Home Loan Switching Charges: ( I have already received refund)

All the charges except procesing fee (around 9000) were refunded by HSBC and Loan Processing agency. They gave me in writing what will be refunded and when.

4. Overall process experience

Home Loan processing expereince with either HDFC or HSBC is very smooth and no hasseles at all. HSBC only looks for higher CIBIL score.

Process of closing Home Loan with HDFC was smooth. They offered lower interest rate only upon closure application.

HDFC also refused to link Interest rates with RBI Repo rate and they said they do not follow this process.

Home Loan switching with HSBC was also smooth and I never visited their branch.

I can share and influence HSBC agency contacts if anyone wants to switch the loan. Keep in mind good Cibil will give you lower rates and rest of the conditions remains same.

If you are from Pune then I can share some direct HSBC contacts who can make this process butter smooth for you.

Considering all the factors and hacing seen my colleagues expereince with HSBC I switched my Home Loan.

Now I have freed myself from the worries of moving interest rates, keeping watch every month and paying extra changes to HDFC for lowering the rates.

Attachments