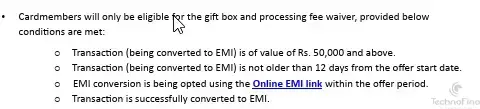

I received an offer on my MRCC card, but the processing fee reversal is capped at 1,000 INR. Let’s evaluate whether converting a 50,000 INR expense into a 3-month EMI (Equated Monthly Installment) is worthwhile based on the provided details:

- **Loan Amount**: 50,000 INR (minimum amount)

- **EMI Tenure**: 3 months (shortest option)

- **Processing Fee**: 2% of the loan amount + 18% GST, with up to 1,000 INR reversed

- **Interest Rate**: 16% per annum

### Step 1: Calculate the Processing Fee

- Processing fee = 2% of 50,000 = 0.02 × 50,000 = 1,000 INR

- GST on processing fee = 18% of 1,000 = 0.18 × 1,000 = 180 INR

- Total processing fee before reversal = 1,000 + 180 = 1,180 INR

- Reversal of processing fee = Up to 1,000 INR (since the fee is exactly 1,000, the entire processing fee is reversed, but the GST of 180 INR is not)

- **Net processing fee** = 1,180 - 1,000 = **180 INR**

### Step 2: Calculate the Interest

- Annual interest rate = 16%

- Tenure = 3 months = 3/12 = 0.25 years

- For simple interest (common for short-term EMIs), interest = Principal × Rate × Time

- Interest = 50,000 × 0.16 × 0.25 = 2,000 INR

- However, EMIs typically use a reducing balance method. For a 3-month tenure, the interest is often approximated as flat. Let’s compute the EMI to confirm.

### Step 3: Calculate the EMI

- Principal = 50, grand000 INR

- Monthly interest rate = Annual rate / 12 = 0.16 / 12 = 0.013333 (1.3333% per month)

- Number of months = 3

**Monthly EMI ≈ 17,276.67 INR**

### Step 4: Total Cost Over 3 Months

- Total amount paid = EMI × Tenure = 17,276.67 × 3 ≈ 51,830 INR

- Interest component = Total paid - Principal = 51,830 - 50,000 = **1,830 INR**

- Total cost = Interest + Net processing fee = 1,830 + 180 = **2,010 INR**

- **Total additional cost**: 2,010 INR (interest + net processing fee) over 3 months, or roughly 4% of the principal.

### Recommendation

If the expenses are genuine and not manufactured, opting for the EMI could be reasonable. Additionally, if the spending helps meet milestones for a Platinum Travel Card, it may be worth considering. However, for the MRCC card, I would not recommend this due to the additional costs involved.