Sumit

TF Buzz

If you ever plan to purchase any financial product from Ola, do go through this article once

This article is regarding a few things:

- How do Postpaid / Buy Now Pay Later kinds of services work

- How regular monitoring of Credit Score is useful not just for financial nerds but for everyone

- What to do in case there are serious issues

- My experience with Ola Money Postpaid

Another important thing that most people are not aware of is that only the lending partner is the one regulated by RBI and not the Frontend/FinTech partner. In case of any issues, the FinTech partner is not liable to do anything, is not required to have a grievance redressal mechanism and can’t be complained against to RBI's Banking Ombudsman.

After a couple of weeks of waiting, Ola finally agreed that this is a mistake from their side and asked for 60 days to correct this. Seriously 60 days!!

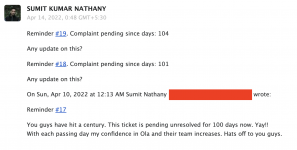

From that time onwards, I have sent 21 Reminder emails to Ola, 9 tweets across a period of almost 4 months. Ola has not done anything at all — no I am not exaggerating — they have not done anything at all. Every single time they have asked for more and more time. I wrote to them multiple times asking me to be included in their communication with their lending partner and what other way I can help to speed things up but they just kept on ignoring these requests and asked for more time without. After a point, they stopped responding to reminders emails. My request is still open to this date and there is no one I can complain to about this. I also wrote to Ola CEO Bhavish Agarwal but no response (frankly speaking, I didn’t expect him to respond as well)

Within 2 weeks of that, late payment disappeared from credit reports of all credit rating agencies. My Credit Score went back to normal in Experian but on CRIF and CIBIL, the score didn’t move much. On CIBIL, it just increased by 7 points whereas it had dropped by almost 40 points. I raised multiple complaints to CIBIL to restore my Credit Score but turn around time from CIBIL was extremely poor — they took more than 30 days to just close my complaint for some random reason. I have raised an escalation for that.

But what worries me the most is how ridiculous and customer insensitive is Ola Money Customer care and their entire team. To this date, Ola is asking for more time to get things resolved 😀.

I am just glad that I didn’t buy a serious product like Health Insurance or Term insurance from Ola. The last thing anyone would want in cases of emergencies is to deal with such a lousy and ridiculous service. This is not the first time I am seeing such mischievous conduct from the Ola group. Even in Ola cabs, their support page to request for reversal of cancellation fee mysteriously doesn't work for weeks. Finally, when it works, they say that a request for reversal of cancellation cannot be taken after a week!!! I have also seen multiple people complaining on Twitter about their Ola Money Postpaid payment page not working and they getting charged late payment fees because of that.

For financial services, most important thing is to have trust and peace of mind. With Ola, I don't have either of that.

This article is regarding a few things:

- How do Postpaid / Buy Now Pay Later kinds of services work

- How regular monitoring of Credit Score is useful not just for financial nerds but for everyone

- What to do in case there are serious issues

- My experience with Ola Money Postpaid

How does Buy Now Pay Later / Post Paid Services work:

Now-a-days, there are a lot of Buy Now Pay Later kinds of services available. For example -- Ola Money Postpaid, Amazon Pay Later, Slice Card, PostPe, PayTM Postpaid, etc. These services are managed by two companies.- Frontend/FinTech partner -- These are companies like Ola, PayTM, and Amazon with which the customer interacts.

- Lending partner -- These are mostly NBFCs (Non-banking financial companies) like Capital Float, Aditya Birla Finance, etc

Another important thing that most people are not aware of is that only the lending partner is the one regulated by RBI and not the Frontend/FinTech partner. In case of any issues, the FinTech partner is not liable to do anything, is not required to have a grievance redressal mechanism and can’t be complained against to RBI's Banking Ombudsman.

My experience with Ola Money Postpaid

I have been handling multiple Credit Cards for the last 10 years and have never missed a payment in any one of them. My CIBIL score used to be 792 (used to be 800+ before CIBIL changed their algorithms). In December last year, I bought a yearly subscription of CIBIL to better monitor my Credit Score. Within a few weeks of that, I saw that my CS dropped by 40 points which has never happened in the past. On checking the report, I found that Aditya Birla Finance had marked one of my payments as late. I realised that this is from Ola Money Postpaid. I quickly checked and confirmed that this was a mistake and I didn’t do a late payment. On the same day, 31-Dec-2021, I sent an email to Ola complaining about this. This is how I spent my new year's eve.After a couple of weeks of waiting, Ola finally agreed that this is a mistake from their side and asked for 60 days to correct this. Seriously 60 days!!

From that time onwards, I have sent 21 Reminder emails to Ola, 9 tweets across a period of almost 4 months. Ola has not done anything at all — no I am not exaggerating — they have not done anything at all. Every single time they have asked for more and more time. I wrote to them multiple times asking me to be included in their communication with their lending partner and what other way I can help to speed things up but they just kept on ignoring these requests and asked for more time without. After a point, they stopped responding to reminders emails. My request is still open to this date and there is no one I can complain to about this. I also wrote to Ola CEO Bhavish Agarwal but no response (frankly speaking, I didn’t expect him to respond as well)

Here is how I got this problem resolved and what you can also do when you face something similar

After Ola continued to ask for more time, I raised a dispute with CIBIL against my Credit Report. That didn’t see much traction though. Finally, I wrote an email to the Banking Ombudsman but they declined to take action since the complaint was not against a regulated entity (Ola in this case). Finally, I formally complained to Banking Ombudsman by filling out a form on their website and raising a complaint against Aditya Birla Finance (ABFL). Within a week, ABFL corrected the mistake, reported it back to all Credit Reporting agencies and their grievance redressal officer called me and confirmed with me. He also told that they have nothing to do with this -- for all Ola Money Postpaid users, they get all the reports and dates from Ola and report that back to Credit Reporting agencies (like CIBIL).Within 2 weeks of that, late payment disappeared from credit reports of all credit rating agencies. My Credit Score went back to normal in Experian but on CRIF and CIBIL, the score didn’t move much. On CIBIL, it just increased by 7 points whereas it had dropped by almost 40 points. I raised multiple complaints to CIBIL to restore my Credit Score but turn around time from CIBIL was extremely poor — they took more than 30 days to just close my complaint for some random reason. I have raised an escalation for that.

Key learnings:

- Regularly monitor your Credit Score and if possible have a subscription to CIBIL's Annual plan. Without this, I would have never found out why my score dropped in the first place.

- If possible, avoid using BNPL services -- the value that you get back is not worth the pain which you suffer in case things go wrong.

- Writing to Banking Ombudsman is sometimes the fastest and the last way to get your problem resolved but only after you have already raised a complaint with the bank

- FinTech partners like Ola/Amazon and others are not regulated and are not responsible to have any grievance redressal mechanism. They do not even have a responsibility to resolve your complaint in the first place and you can't complain against that anywhere (maybe in consumer court but very few of us have the time and money to do that)

But what worries me the most is how ridiculous and customer insensitive is Ola Money Customer care and their entire team. To this date, Ola is asking for more time to get things resolved 😀.

I am just glad that I didn’t buy a serious product like Health Insurance or Term insurance from Ola. The last thing anyone would want in cases of emergencies is to deal with such a lousy and ridiculous service. This is not the first time I am seeing such mischievous conduct from the Ola group. Even in Ola cabs, their support page to request for reversal of cancellation fee mysteriously doesn't work for weeks. Finally, when it works, they say that a request for reversal of cancellation cannot be taken after a week!!! I have also seen multiple people complaining on Twitter about their Ola Money Postpaid payment page not working and they getting charged late payment fees because of that.

For financial services, most important thing is to have trust and peace of mind. With Ola, I don't have either of that.

Attachments