curios_mind_huh

TF Select

I just made a purchase on Amazon with my HDFC Millennia credit card that saved me Rs.10,000 in instant discount and an additional Rs.4,500 in No-Cost EMI discount. The processing fee is Rs.353 and the foreclosure charge comes out to Rs.2000. Even if I foreclose the EMI without waived charges, I'll still be in the gains because of the huge upfront No-Cost EMI discount.

This is where the dilemma starts. I've already read all the posts here about the foreclosure charges levied by HDFC. I made a similar EMI transaction with HDFC on 4th December,2024 and fore-closed the EMI via MyCards as soon as it got converted. Despite what everyone said, HDFC did not charge foreclosure fee (even though it was mentioned in MyCards app) and even refunded the processing fee (without GST). What more, contrary to the popular belief the instant discount on EMI wasn't reversed till now as well.

I don't know if much has changed from then. I'm okay paying the processing and foreclosure fee for EMI cancellation. But if HDFC really does reverse the Rs.10,000 instant discount, it absolutely does not make any sense to cancel the EMI. Does HDFC really do this and Has anyone experienced this?

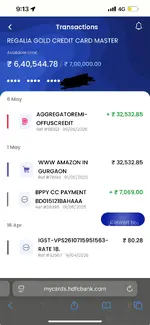

Update: I pre closed the EMI from mycards on May 1, 2025. When I went through terms and conditions, there was indeed a clause that stated "No charges apply in case EMI is closed within 3 days". HDFC also asked me to settle the whole principal, charges and processing fee within the next day and I did so as well. The processing fee was reversed, it's GST was not and no pre-closure charges were debited as of today.

There are terms and conditions which state the instant discount will get debited within 120 days, but I hope not. I'll update this space after 120 days if HDFC decides to cancel the instant discount.

Update to everyone: I closed two ongoing NCEMI with HDFC. Preclosure charges + GST (3.54%) was levied, but I got it back after 5 working days. From their official documentation webpage https://www.hdfcbank.com/personal/borrow/popular-loans/easy-emi/easyemi-on-consumer-durables, " In case the loan is pre-closed within 3 days of loan booking date, any pre- closure fees levied will be reversed within 15 working days".

I raised an email to their priority redressal team and this is their reply: "since it was closed within 3 days timelines, we have exceptionally reversed the Processing fee & Preclosure fee along with GST to your card account"

But I'm still not sure if the instant discounts will be reversed as well. Will have to wait out another 120 working days to check if it's really the case.

This is where the dilemma starts. I've already read all the posts here about the foreclosure charges levied by HDFC. I made a similar EMI transaction with HDFC on 4th December,2024 and fore-closed the EMI via MyCards as soon as it got converted. Despite what everyone said, HDFC did not charge foreclosure fee (even though it was mentioned in MyCards app) and even refunded the processing fee (without GST). What more, contrary to the popular belief the instant discount on EMI wasn't reversed till now as well.

I don't know if much has changed from then. I'm okay paying the processing and foreclosure fee for EMI cancellation. But if HDFC really does reverse the Rs.10,000 instant discount, it absolutely does not make any sense to cancel the EMI. Does HDFC really do this and Has anyone experienced this?

Update: I pre closed the EMI from mycards on May 1, 2025. When I went through terms and conditions, there was indeed a clause that stated "No charges apply in case EMI is closed within 3 days". HDFC also asked me to settle the whole principal, charges and processing fee within the next day and I did so as well. The processing fee was reversed, it's GST was not and no pre-closure charges were debited as of today.

There are terms and conditions which state the instant discount will get debited within 120 days, but I hope not. I'll update this space after 120 days if HDFC decides to cancel the instant discount.

Update to everyone: I closed two ongoing NCEMI with HDFC. Preclosure charges + GST (3.54%) was levied, but I got it back after 5 working days. From their official documentation webpage https://www.hdfcbank.com/personal/borrow/popular-loans/easy-emi/easyemi-on-consumer-durables, " In case the loan is pre-closed within 3 days of loan booking date, any pre- closure fees levied will be reversed within 15 working days".

I raised an email to their priority redressal team and this is their reply: "since it was closed within 3 days timelines, we have exceptionally reversed the Processing fee & Preclosure fee along with GST to your card account"

But I'm still not sure if the instant discounts will be reversed as well. Will have to wait out another 120 working days to check if it's really the case.

Last edited: