Have you ever wondered how credit card companies make money? They offer you a credit card, and you use it for your purchases, paying your bill on time. In return, they provide you with reward points, cashback, and enticing lifestyle benefits like airport lounge access and free golf. But how do they manage to offer all these perks? Who is actually footing the bill for these rewards and benefits? Let’s delve into some intriguing questions about the credit card business and find the answers.

TF Community Thread Link For Discussion: https://www.technofino.in/community/threads/understanding-the-business-of-credit-cards-exploring-revenue-models-and-the-funding-behind-your-free-vacation-through-card-rewards.14127/

How do credit card companies make money? What are the main sources of income for a credit card company?

A credit card company functions as a lending business, similar to other lending enterprises, where credit card companies earn profits by providing loans. However, unlike traditional lending businesses, credit card companies generate revenue not only from interest income but also from three other significant sources of income. These sources include:

- Interest Income:

Similar to other lending businesses, credit card companies generate interest income by levying interest on the outstanding balances carried by cardholders on their credit cards. When a customer fails to make timely payments or pays only a portion of the total bill, credit card companies apply interest charges on the remaining balance. These interest rates are generally high, typically ranging from 30% to 50% per annum.

In addition, if a customer chooses to make a purchase through an Equated Monthly Installment (EMI) plan, the credit card company applies interest on the financed amount. In such cases, the interest rates are typically lower, ranging from 10% to 20% per annum.

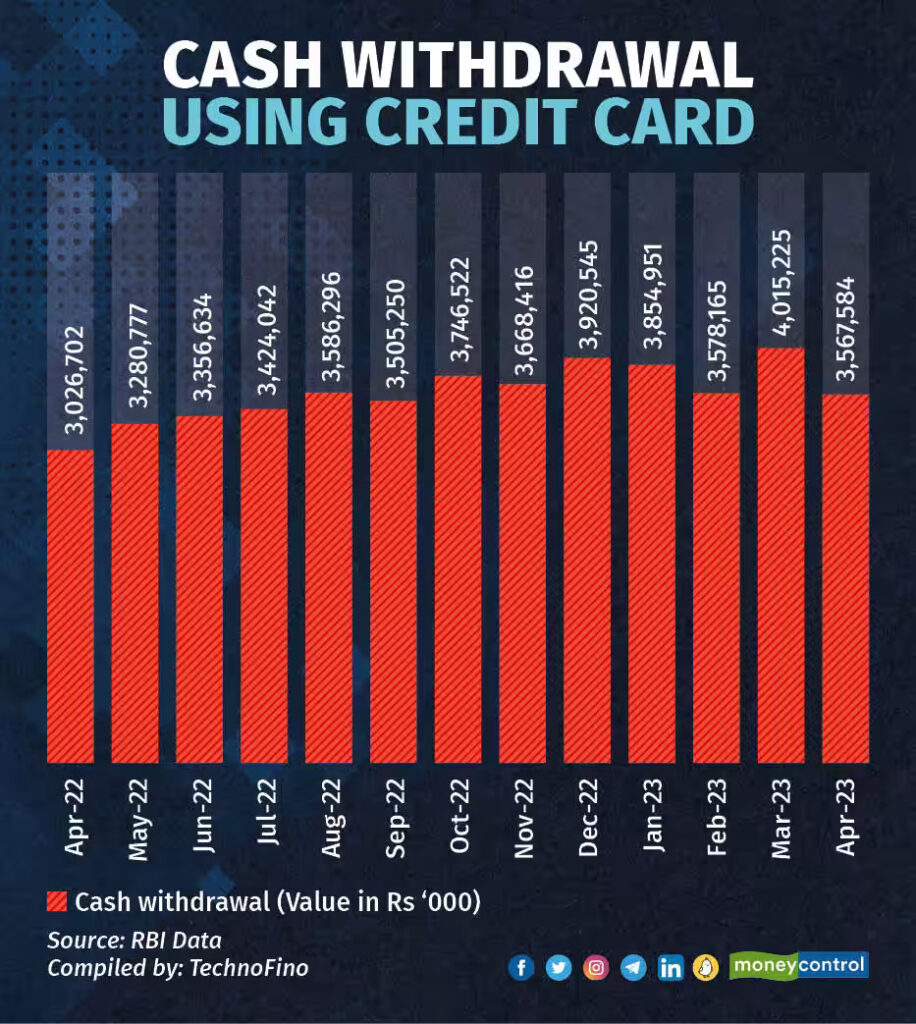

Furthermore, if someone withdraws cash using a credit card, the card issuer charges interest on the withdrawn amount, along with associated fees. While you may wonder who would withdraw cash using a credit card, it is interesting to note that according to RBI data, Indian consumers have consistently withdrawn amounts ranging from Rs. 300 to Rs. 400 crores each month, from April of the previous year to April of this year.

It is important for cardholders to be aware of the interest rates associated with their credit cards and to make timely payments to avoid accruing high interest charges.

- Interchange Income:

Credit card companies generate revenue through interchange income in addition to interest income. Merchant Discount Rate (MDR) fees are charges imposed on merchants when they accept credit card payments. These fees are typically calculated as a percentage of the transaction value, ranging between 1% and 3%. The MDR income is distributed among various parties in the payment ecosystem, including the acquiring bank (which processes the merchant’s card transactions), the card issuing bank (which issued the credit card to the customer), and the card network (such as Visa, Mastercard, or American Express) that facilitates the transaction. Interchange fees, charged by the card issuer, usually represent the largest proportion of the overall MDR. - Membership Fees:

Another source of income for credit card companies is membership fees. When customers apply for and are approved for a credit card, the bank may require them to pay a one-time joining fee. Additionally, credit card companies charge annual fees to cardholders. The specific amount of the annual fee depends on the features, benefits, and rewards associated with the card. Premium credit cards, which offer enhanced perks such as travel rewards, concierge services, or exclusive access to events, often carry higher annual fees. - Other Fee-based Income:

In addition to interest income, interchange income, and membership fees, credit card companies earn revenue through various other fees. These fees may include balance transfer fees, late payment fees, cash advance fees, foreign transaction fees, and other charges associated with specific services or transactions.

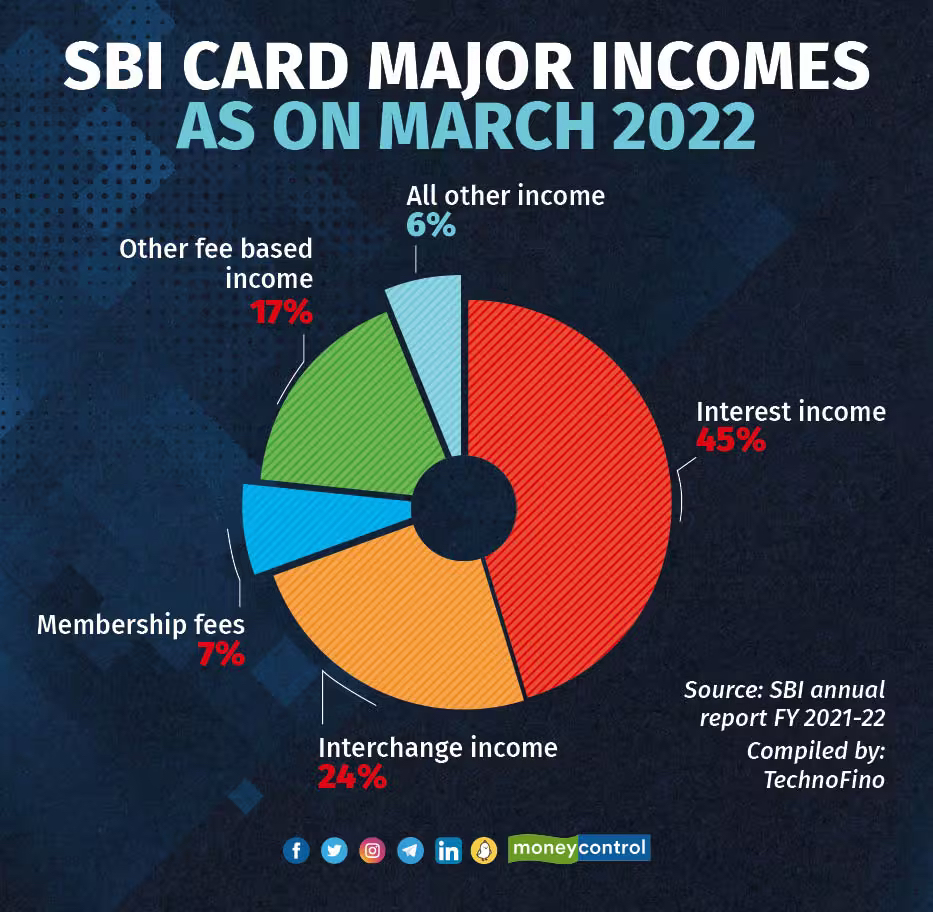

To gain insights into the income sources of credit card companies, let’s examine the income distribution of SBI Card for the fiscal year 2021-2022. SBI Card, the second-largest card issuer in India, generated the following revenue streams:

Based on these figures, it can be observed that 45% of SBI Card’s income is derived from interest charged to its customers. An additional 24% comes from interchange fees collection, which is the fee charged to merchants. Another 24% is generated from credit card membership fees and other related charges. The remaining 6% is contributed by various other income sources.

Who actually pays for credit card rewards?

We often utilize credit cards to take advantage of various rewards offered, such as cashback, reward points, and airmiles. But have you ever wondered why credit card companies incentivize us to use their cards? The answer lies in the financial benefits they derive from our spending habits.

Credit card companies earn revenue through several means, and one significant source is the Merchant Discount Rate (MDR) fees paid by merchants. The more we spend using their credit cards, the more income credit card companies generate from these fees. Additionally, increased spending also raises the likelihood of delayed payments, resulting in interest income for banks.

To encourage customers to spend more, banks and credit card companies frequently send targeted offers to their customers and promote discounted online/offline sales. By doing so, they aim to increase customer spending, leading to higher revenue.

If we take a closer look at SBI Card’s financial report for the fiscal year 2021-2022, we can observe that they spent Rs. 622.63 crores for customer rewards (reward redemption cost). This amount accounts for approximately 5.81% of their total income and around 15% of their total operational expenses.

Hence, it can be inferred that individuals who delay payments, carry balances on their credit cards each month, or make purchases through EMIs effectively finance the credit card rewards and perks enjoyed by other customers.

What are the major expenses of a credit card company?

Managing a credit card company entails significant costs, with various expenses associated with its operations. Some key expenditures include interest expenses incurred from borrowing money, managing bad debt and write-offs, maintaining reward programs, and investing in advertising and sales promotion.

I have consulted with bank officials from some of the top Indian credit card companies, and they have identified advertising and sales promotion, rewards and loyalty programs, collection of dues, and IT-related expenses as their major expenditures.

What would happen if all customers started paying their credit card bills on time? Would credit card companies be able to survive such situations?

If all customers start paying their 100% bill on time then It’ll make more damage than good. It will reduce bad loans, improve cashflow, but credit card companies heavily rely on interest income and late payment fees. As stated earlier, almost 40 to 60% income of a credit card company comes from interest & other related fees.

In such a scenario, credit card companies would need to adapt their business models and strategies to compensate for the potential loss of revenue from interest charges and late payment fees. They might explore new avenues to generate income or adjust their fee structures and rewards programs accordingly. Additionally, they would need to carefully manage costs and optimize their operational efficiency to maintain profitability.

During discussions with officials from top credit card companies, they said, “All customers paying their bills in full on time is a thought experiment, just like all policyholders claiming insurance at the same time. Two things can happen in this case. The credit card business will become commoditized, with low margins and only a few big players surviving. “The Indian market will then begin to mimic the characteristics of the card market in developed economies.”

In conclusion, a credit card can be a valuable financial tool when used responsibly. However, the irony lies in the fact that if you are a responsible consumer, you may not be as profitable for the credit card company. Finding a balance is essential because we cannot expect everyone to default on their payments or pay their bills on time. Credit card companies require a mix of responsible users who pay their bills on time and users who carry forward balances, allowing them to earn interest and maintain cash flow. Striking a balance between these user types is crucial for the sustainability and profitability of credit card companies.

Meet Sumanta Mandal, the founder of Technofino, a renowned platform dedicated to providing valuable insights on credit cards and other banking products. With a profound knowledge of credit cards, Sumanta specializes in analyzing credit card reward systems and airmiles. His passion for the credit card industry drives him to delve deep into the intricacies of various credit card programs and uncover the best strategies to maximize rewards.

{kind=link}